Oracle’s Earnings Reveal the Real AI Bottleneck: Cloud Capacity

- JENNY LEE

- Mar 10

- 3 min read

AI demand is real. Deliverable capacity is the constraint.

Summary

Oracle’s latest earnings confirm that the AI cycle is entering a new phase.

Demand for AI infrastructure continues to surge, but the limiting factor is no longer only semiconductors. The real constraint is the ability to deliver cloud capacity at scale.

Oracle’s massive backlog growth and accelerating OCI expansion suggest the company is becoming a key allocator of AI compute capacity within the enterprise ecosystem.

Oracle’s latest earnings triggered a sharp rebound in the stock after a steep pullback. At first glance the move looks dramatic. But both the fundamentals and the long-term market structure tell a more nuanced story.

The quarter was undeniably strong.

Oracle reported fiscal Q3 revenue of $17.2 billion, up 22% year over year, while total cloud revenue rose 44% to $8.9 billion. OCI — the infrastructure segment most tied to AI workloads — surged 84% to $4.9 billion. Meanwhile, Remaining Performance Obligations reached $553 billion, a 325% increase from the prior year.

Those numbers confirm something important: AI demand is no longer theoretical. It is now translating into long-duration enterprise contracts.

But the significance of the quarter goes beyond the headline growth.

For most of the past two years, the AI narrative has been dominated by the semiconductor layer. More GPUs, more training clusters, more chip supply constraints. Oracle’s results suggest the bottleneck may now be shifting further up the stack — toward deliverable cloud capacity.

Management made it clear that demand for AI training and inferencing continues to grow faster than supply. More importantly, many of the large AI agreements driving the surge in backlog are structured in ways that reduce Oracle’s financing burden: in some cases customers prepay for capacity, while in others they supply the GPUs themselves.

This effectively turns part of the cloud infrastructure business into something closer to contracted infrastructure delivery rather than speculative capacity expansion.

In other words, Oracle is not simply selling software anymore.

It is increasingly allocating AI compute capacity under long-term enterprise contracts.

That distinction matters.

It suggests the company is positioning itself somewhere between hyperscale cloud providers and traditional enterprise software vendors — a hybrid model that connects infrastructure, databases, and enterprise workloads into a single ecosystem.

Still, the risks remain visible.

Oracle reaffirmed $50 billion in capital expenditures for fiscal 2026, and the company has significantly increased financing to support its infrastructure expansion. This means the debate around Oracle is likely to shift between two competing narratives over the coming quarters: the strength of AI demand versus the sustainability of the capital structure required to support it.

For now, the demand side appears to be winning that argument.

The Technical Structure Tells a Similar Story

The recent decline in Oracle’s share price appears severe on short-term charts. But when viewed from a longer-term perspective, the move looks far less dramatic.

On a monthly time frame, Oracle has followed a remarkably consistent pattern since the aftermath of the global financial crisis: strong multi-year advances followed by periodic mean-reversion toward its long-term moving average.

Each major pullback over the past fifteen years — in 2011, 2016, 2020, and 2022 — ultimately returned to the same structural anchor: the long-term trend line represented by the 50-month moving average.

The current decline is occurring in exactly the same area.

What makes the recent move appear more violent is the steep acceleration in the stock during the AI rally of 2023–2025. When prices rise far above their long-term trend, the eventual reversion toward that trend can feel like a collapse on shorter time horizons.

But structurally, the pattern remains familiar.

This is not yet a breakdown of the long-term trend. It is a reset after a period of unusually rapid expansion.

A Different Phase of the AI Cycle

Taken together, Oracle’s earnings and its long-term price structure point toward a broader transition in the AI investment cycle.

The early phase of the cycle was defined by semiconductor scarcity. The next phase may be defined by something more operational: the ability to convert AI demand into deployed infrastructure, signed contracts, and recurring enterprise workloads.

Oracle’s latest quarter does not prove that it will dominate that transition. But it does confirm that the company is already participating in it.

AI is no longer only about who builds the chips.

Increasingly, it is about who can turn AI demand into delivered capacity.

Oracle now sits squarely inside that layer of the stack.

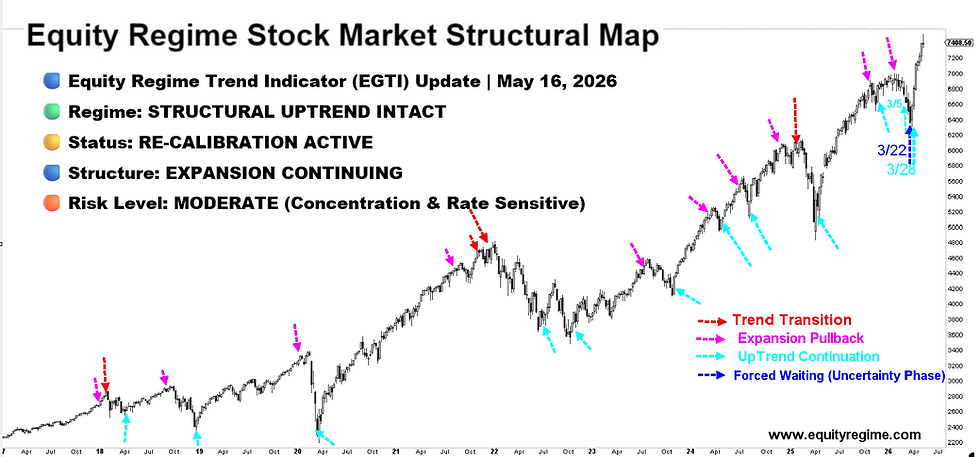

Chart1:Oracle Long-Term Monthly Structure

Despite the recent sharp decline, Oracle remains within its long-term uptrend.

Historically, pullbacks toward the 50-month moving average have acted as structural resets after periods of accelerated growth.