Real Estate Is Back: From Collapse Narrative to Macro Re-Rating

- JENNY LEE

- Feb 21

- 3 min read

Updated: Feb 23

For nearly two years, real estate remained one of the market’s most abandoned sectors. Rising interest rates, refinancing risks, and persistent crisis narratives drove positioning to extreme underweight levels, leaving REIT valuations structurally compressed.

That regime is now shifting.

Recent market behavior suggests the sector is transitioning from distressed pricing toward an early-stage re-rating phase supported by improving breadth, stabilizing rates, and a structural reduction in liquidity-driven downside risk.

Price Structure: Sector-Wide Breakout

Major real estate ETFs — $IYR, $VNQ, and $XLRE — are advancing in tandem, breaking out of multi-month consolidation ranges. The synchronized behavior across these benchmarks indicates that recent strength reflects asset-class level capital inflows rather than isolated stock-specific catalysts.

This alignment typically marks the early stage of sector rotation, where capital repositioning outweighs incremental fundamental change.

Breadth Confirmation: Participation Is Expanding

The S&P Real Estate Bullish Percent Index ($BPREAL) has risen sharply from depressed levels, reclaiming the 50% threshold and moving into bullish participation territory. This development carries critical implications:

Increasing numbers of REIT components are generating active buy signals

Internal sector health is improving

The rally is broadening rather than narrowing

Price strength accompanied by breadth expansion is a classic signature of early normalization cycles.

Chart 1: S&P Real Estate Bullish Percent Index

The chart highlights a decisive recovery in sector participation, reinforcing the view that the current advance is not driven by a narrow subset of assets but reflects improving internal market structure.

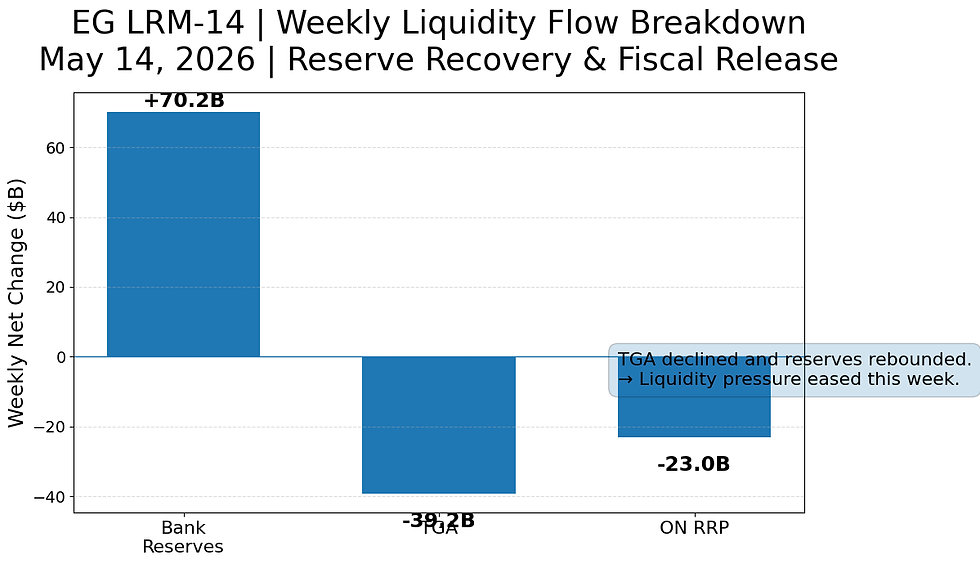

Liquidity Anchor: The EG LRM-14 Perspective

The structural recovery in REIT pricing is consistent with a liquidity floor rather than a liquidity expansion dynamic.

Under the EG LRM-14 framework, the system has transitioned into a Re-calibration Regime characterized by stable reserve balances and a significant reduction in liquidity drainage. Bank Reserves remain anchored near critical thresholds while ON RRP usage has largely been exhausted, removing a major source of systemic liquidity absorption.

This environment reduces downside convexity for duration-sensitive assets, allowing valuations to reprice without requiring an outright liquidity expansion cycle.

Rate Inflection: Mortgage Costs and Refinancing Pressure

The U.S. 30-year fixed mortgage rate has declined to its lowest level since October 2022, marking a meaningful shift in the sector’s macro backdrop.

Given real estate’s long-duration cash flow profile, mortgage rates serve as the primary transmission channel between monetary conditions and property valuations. A sustained easing in financing costs reduces refinancing pressure, improves transaction feasibility, and stabilizes asset pricing expectations.

Chart 2: U.S. 30-Year Fixed Mortgage Rate

The chart illustrates the peak-to-decline dynamic in mortgage rates, signaling the exhaustion of the duration-risk premium that has weighed on real estate valuations for nearly two years.

ETF Leadership: Public Markets Lead the Property Cycle

Historically, public REITs lead underlying property price cycles by six to nine months, reflecting forward-looking capital allocation rather than contemporaneous property fundamentals.

The synchronized advance in $IYR, $VNQ, and $XLRE suggests that capital markets are beginning to discount improving macro conditions ahead of observable changes in private-market appraisals. This forward-looking behavior implies that while physical real estate pricing may remain stagnant in the short term, the equity re-rating has already begun.

Commercial Real Estate: Structural Bifurcation

While structural challenges persist across specific subsectors, market pricing indicates that the systemic crisis narrative is approaching exhaustion.

The sector is undergoing structural bifurcation:

Legacy Office Assets remain in a cleansing phase, burdened by structural vacancy and refinancing stress

Data Centers, Logistics, and specialized REITs are entering premium expansion cycles driven by durable cash flows and structural demand

This transition reflects a shift from systemic collapse risk toward asset-level differentiation.

Conclusion

Real estate is no longer trading as a distressed asset class. Driven by mortgage rate easing, breadth expansion, and the stabilization of systemic liquidity conditions, the sector is entering a phase of macro re-rating.

While the path forward is unlikely to be linear—particularly in a buffer-constrained liquidity environment—the combination of positioning asymmetry and forward-looking capital flows suggests that real estate is evolving from a neglected segment into a credible rotation candidate within the broader equity market.

The evidence indicates that the crisis narrative has largely been priced, and the sector is transitioning toward normalization dynamics with ETF leadership preceding improvements in underlying property valuations.