When Tesla Stops Explaining the Index

- JENNY LEE

- Jan 29

- 3 min read

This is not a trade idea. It is a review of signal reliability when market narratives become unstable.

Why TSLA needs to be treated differently

TSLA has never been just another large-cap stock.

At different points in the cycle, it has acted as a proxy for growth optimism, a volatility outlet, and occasionally a vessel for collective belief.

That versatility is precisely why TSLA becomes dangerous to interpret during periods of extreme divergence.

When an asset simultaneously carries narrative density, liquidity concentration, and emotional projection, its price action can look decisive while quietly losing informational value.

This article is not about whether TSLA is bullish or bearish.

It is about when TSLA’s behavior stops telling us anything reliable about the broader market.

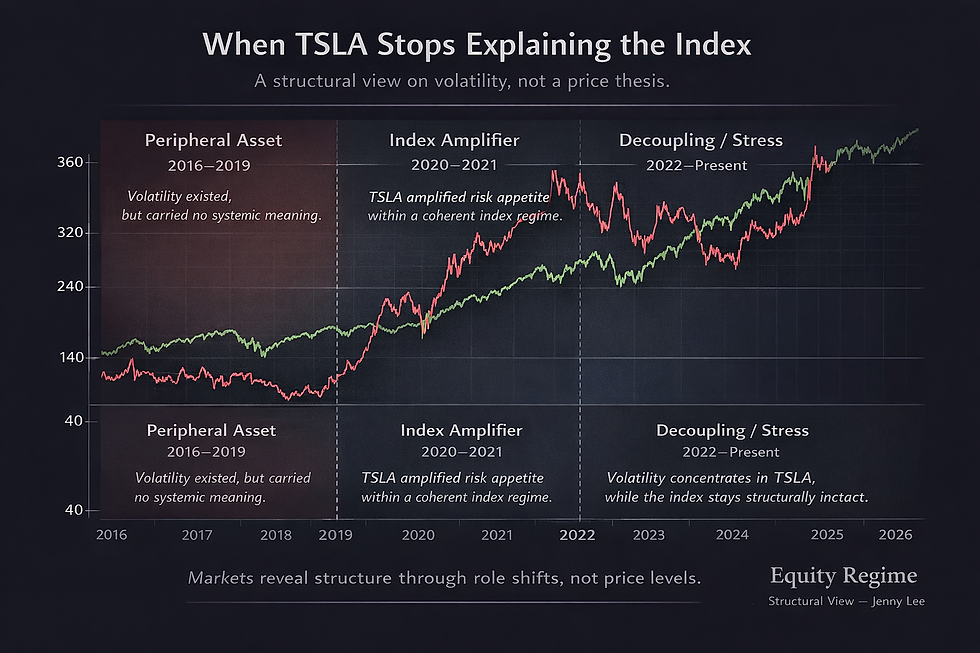

Phase I (2016–2019): Volatility without systemic meaning

Between 2016 and 2019, TSLA was volatile, erratic, and often dramatic.

But critically, its movements did not alter the structure of the index.

The Nasdaq continued its trend with little regard for TSLA’s drawdowns or rallies.

TSLA’s volatility was tolerated, not absorbed.

This distinction matters.

Volatility that is not absorbed by the system remains peripheral noise.

It may be painful or exciting for holders, but it carries no message about systemic risk.

At this stage, TSLA was optional volatility — allowed, but not consequential.

Phase II (2020–2021): TSLA as an index amplifier

The role changed decisively in 2020.

TSLA’s acceleration did not occur outside the index structure; it occurred within it.

Risk appetite was coherent, liquidity abundant, and index participation broad.

TSLA’s function during this period was not to lead the market independently, but to amplify what the index was already expressing.

This distinction is subtle but essential.

When an asset amplifies an existing regime, its volatility strengthens the signal rather than distorting it.

TSLA’s outsized moves were not warnings; they were confirmations of a synchronized risk-on environment.

During this phase, TSLA mattered — but only as a multiplier, not as a compass.

Phase III (2022–Present): Decoupling and stress concentration

The most important shift occurred after 2021.

From 2022 onward, TSLA’s volatility began to concentrate internally, while the index demonstrated increasing structural resilience.

Drawdowns in TSLA became deeper, rebounds more erratic, and directionality less consistent — all without triggering corresponding instability in the Nasdaq.

This is the defining feature of the current regime:

Volatility concentrates in TSLA, while the index remains structurally intact.

When this happens, TSLA stops “explaining” the market.

Its price swings reflect internal conflict — positioning, narrative repricing, and emotional rebalancing — rather than changes in systemic risk.

This is not weakness.

It is a change in function.

Why I deliberately reduce conclusion density in this regime

Periods of decoupling are not environments for confident directional calls.

They are environments for signal discipline.

When signals fragment — price action pointing one way, structure pointing another — the primary risk is not being wrong.

It is becoming prematurely certain.

In these regimes, I care less about where TSLA trades next and more about which signals remain consistent across assets.

Structure outlasts sentiment.

Roles outlast narratives.

What this framework is — and is not

This framework is not designed to forecast TSLA’s next move.

It is designed to prevent misattribution.

When a high-volatility leader detaches from the index, interpreting its movement as a market verdict becomes a category error.

Markets do not always weaken when leaders wobble.

Sometimes, they simply stop using those leaders to communicate.

Why this matters beyond TSLA

This article is not about TSLA.

It is about recognizing role shifts — moments when a widely watched asset transitions from signal to stress container.

Market leaders change.

Narratives rotate.

But the way noise disguises itself as information is remarkably consistent.

Understanding that distinction is not about trading advantage.

It is about structural survival.

Equity RegimeStructural View — Jenny Lee