2022: The Most Misread Reckoning in Modern Equity Markets

- JENNY LEE

- Feb 5

- 4 min read

The Rewiring of Equity Valuation Frameworks and the Birth of a New Market Order

Beneath the Surface

Most investors continue to interpret 2022 as a cyclical correction triggered by aggressive rate hikes.Such a view understates the magnitude of what actually occurred.

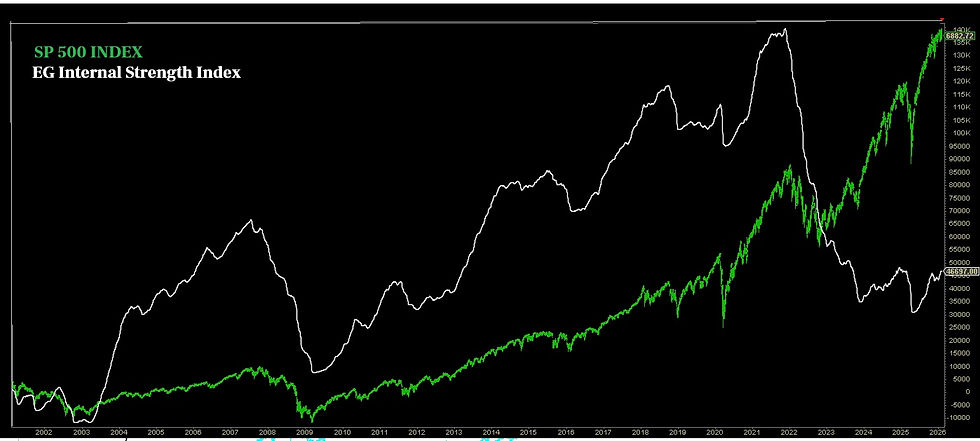

Viewed through the lens of equity market structure — and supported by breadth data from the EG Internal Strength Index — 2022 was not a conventional bear market. It was closer to a systemic reckoning, one whose scope and depth exceeded prevailing market perception at the time.

This episode did more than compress valuations.

It altered the framework through which capital is priced.

Indexes can recover.

But once a valuation regime shifts, the consequences tend to persist.

I. The Echo of 1980 — A Generational Psychological Reset

To understand the significance of 2022, one must look beyond price action and examine sentiment structure.

A rare divergence has emerged:

The S&P 500 trades near historical highs, while the University of Michigan Consumer Sentiment Index remains depressed, hovering near levels typically associated with recessionary conditions.

This combination — resilient asset prices alongside fragile public confidence — was last observed at scale during the Volcker tightening cycle of the early 1980s.

At that time, the violent upward repricing of interest rates did more than suppress inflation. It dismantled the psychological assumptions of an era and forced markets to re-accept a fundamental principle: capital has a cost.

The parallels to 2022 are notable:

The fastest rate-hiking cycle in four decades

Rapid multiple compression

A sharp decline in investor risk tolerance

This was not ordinary volatility.

It was the return of financial gravity.

II. 2000 and 2008 — Why 2022 Was Structurally Different

The bear market of 2000 was largely a technology bubble unwind, concentrated in internet equities. Traditional sectors retained relative stability.

The crisis of 2008 originated within the financial system itself; its destructive force was rooted in credit structures rather than a broad invalidation of corporate profitability.

By contrast, the defining characteristic of 2022 was breadth.

Consumer sentiment fell below 50 and remained suppressed — a contraction in confidence historically comparable only to the early 1980s.

Meanwhile, the collapse of the EG Internal Strength Index breached structural floors that had held for over a decade.

The implication is difficult to ignore:

What was being cleared was not merely excess valuation — but an entire ecosystem dependent on near-zero capital costs.

Financing-driven growth lost market sponsorship.

Efficiency, cash flow, and durability re-emerged as primary valuation anchors.

This is the hallmark of a valuation reset.

III. The Silent Extinction — Market Ecology Rewritten

The breadth deterioration of 2022 represented a restructuring of the equity ecosystem.

For more than a decade, abundant liquidity allowed a wide range of business models to coexist. When the cost of capital abruptly repriced, that equilibrium broke.

Many firms did not fail operationally — but they lost access to inexpensive financing, which in modern markets can be equally decisive.

Importantly, such structural clearing does not always coincide with catastrophic index declines. Mega-cap balance sheet strength helped stabilize headline benchmarks, masking the scale of internal liquidation.

Yet from a structural perspective, the episode resembled earlier periods in which markets restored their selection mechanisms.

Capital stopped subsidizing narratives.

Markets resumed rewarding survivability.

What appeared chaotic was, in fact, disciplinary.

IV. Pricing Polarization and the Emergence of a Durability Premium

The current divergence between the Nasdaq-100 and the EG Internal Strength Index is frequently interpreted as fragility.

It may instead signal a migration of pricing power.

Following systemic repricing, capital rarely disperses evenly. It consolidates around firms demonstrating durability — earnings visibility, pricing power, and structural participation in productivity expansion, increasingly shaped by artificial intelligence.

The market has quietly raised its admission threshold:

Firms lacking sustainable cash flow have been marginalized

Profitability visibility has become central to valuation

Companies possessing technological moats command persistent premiums

Recent index highs are therefore not the product of indiscriminate speculation.

They reflect concentrated profitability among high-quality survivors.

Markets are no longer rewarding possibility.

They are rewarding certainty.

V. The Present Structure — Systemic Discipline, Localized Excess

If 2022 constituted a deep structural purge, an important implication follows:

Systemic bubble risk appears materially reduced.

This does not imply the disappearance of risk. Localized excess is an enduring feature of capital markets, particularly in sectors benefiting from strong secular narratives.

Such overheating, however, typically resolves through sector rotation and valuation normalization rather than systemic collapse.

The recent repricing within segments of the software sector illustrates this mechanism — capital reallocating risk rather than abandoning equities altogether.

Short-term volatility should therefore be interpreted with care:

Not as evidence of structural fragility, but as the market recalibrating pockets of excess.

The distinction is critical for asset allocation.

Conclusion — New Orders Are Often Born from Misread Liquidations

The historical importance of 2022 may lie less in its classification as a bear market and more in its redefinition of how capital is priced.

Misread liquidations often prove the most consequential. They remove systemic vulnerabilities while leaving behind a more efficient, quality-oriented market backbone.

As internal participation gradually stabilizes, the market appears to be transitioning toward a phase of higher-quality expansion.

Investors who continue to interpret divergence itself as risk may find themselves navigating the present with an outdated map — and, in doing so, risk overlooking one of the defining structural shifts of this cycle.

Markets rarely recalibrate twice within the same cycle.

**In equity markets, we do not predict volatility.

We define it.**

Equity Regime

Market structure, risk tolerance, and regime classification