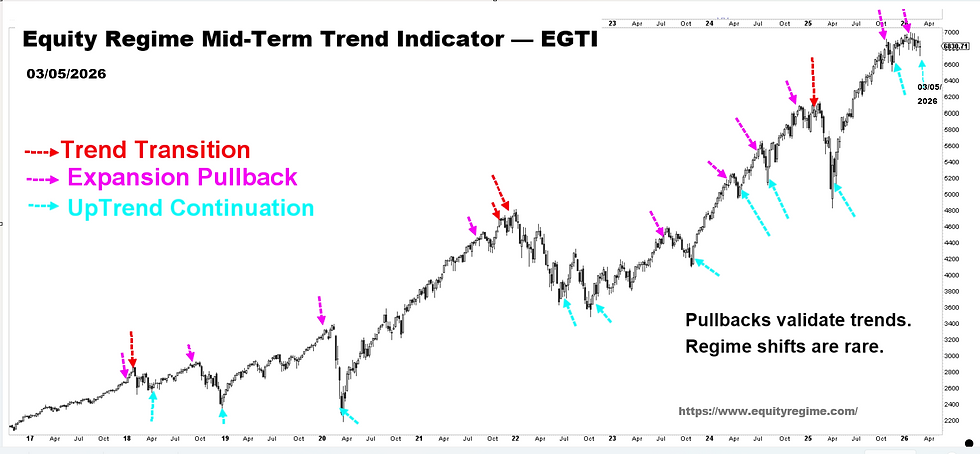

EGTI Weekly Trend Indicator — Updated 03/05/2026

- JENNY LEE

- Mar 5

- 3 min read

Equity Regime Stock Market Mid-Term Trend Indicator

Market State

Re-acceleration attempt within volatility re-calibration

Regime

Structural Uptrend Preserved

Risk Structure

Event-driven volatility interacting with stable liquidity conditions

Verdict

Trend intact.

Volatility normalization interacting with leadership rotation.

No evidence of structural distribution or downside regime transition.

Indicator Note

EGTI is designed as a trend indicator rather than a precise turning-point signal.

Uptrend Continuation signals may still be followed by short-term price weakness, while Pullback signals can occur before the final high of a move. This reflects the leading nature of the framework, as EGTI typically anticipates structural trend developments one to two weeks before they fully manifest in price action.

Founder’s Note — Weekly Structural Update

Market behavior during the week continued to reflect volatility repricing rather than deterioration in the underlying trend structure. Geopolitical headlines introduced episodic volatility across risk assets, yet price behavior at the index level remained consistent with consolidation rather than directional breakdown.

An important structural observation highlighted in the February 19 EGTI note was the early indication of capital rotation toward technology leadership. At that time, cross-index behavior suggested liquidity was gradually reallocating from previously extended cyclical segments into the Nasdaq complex.

Subsequent market price action has now validated this expectation. Relative strength within Invesco QQQ Trust has stabilized while rotational pressure in SPDR Dow Jones Industrial Average ETF Trust and SPDR S&P 500 ETF Trust has moderated.

Current behavior suggests the rotational adjustment is entering its late phase, with leadership realignment increasingly absorbed by the broader market structure.

Breadth dynamics show ongoing normalization across previously extended segments. Bullish percent readings within $XLP (Staples), $XLB (Materials), and $XLI (Industrials) continue to retreat from elevated levels reached earlier in the quarter. Importantly, this moderation has not translated into index-level price weakness, suggesting redistribution of participation rather than broad market deterioration.

Rotation activity has become more visible across leadership groups. $XLF (Financials) and $IGV (Software) continue to demonstrate relative resilience, while weakness within semiconductors led by $NVDA during late-week trading reflects tactical positioning adjustments rather than structural leadership failure. Capital flows within the Nasdaq complex remain internally rotational rather than externally distributive.

Positioning indicators point to continued moderation across both institutional and retail exposures. Although aggregate positioning remains historically elevated, the gradual compression observed over recent weeks indicates a controlled reduction in leverage rather than disorderly liquidation. Such positioning behavior is characteristic of expansion phases transitioning through volatility recalibration.

Sentiment conditions have become increasingly sensitive to short-term volatility. Rising bearish readings within AAII surveys appear primarily linked to recent price fluctuations and geopolitical developments rather than a structural reassessment of risk. Historically, elevated bearish sentiment during consolidation periods tends to coincide with continuation environments rather than regime transitions.

Liquidity conditions monitored through the EGLRM-14 matrix remain stable. Reserve balances continue to anchor the system near the $3T threshold, while Treasury cash flows have modestly injected liquidity into the banking system. With the ON RRP facility now largely exhausted, liquidity transmission occurs more directly through reserve channels. A full EGLRM-14 liquidity update will be provided in the weekly liquidity report.

EGTI Structural Interpretation

The composite EGTI framework continues to classify current market behavior as consolidation within an intact structural advance. The recent increase in volatility reflects normalization following an extended period of suppressed price movement rather than deterioration of the broader trend architecture.

Forward path assessment suggests a modestly higher probability of upside resolution into the coming week as rotational pressures stabilize. Any such advance should be interpreted as continuation within the prevailing expansionary regime rather than emergence of a new trend phase.

Structure remains intact.

Rotation persists.

Trend integrity preserved.

About Equity Regime

Equity Regime is an independent research platform dedicated to mapping structural shifts across markets, technology, and capital cycles.

Our focus is not on predicting daily price movements, but on identifying regime transitions — periods when consensus narratives lag underlying reality and long-term repricing quietly begins.

In an environment dominated by noise, our objective is simple:

Detect the shift before it becomes obvious.